Corporations in Suspension is what happens when a corporation loses its right to legally operate — and for a church or nonprofit, that can mean a pending property sale grinds to a halt overnight. Forming a corporation isn’t a one-time task. Staying in good standing with the California Secretary of State (SOS) and the Franchise Tax Board (FTB) requires ongoing filings, and missing them is what triggers corporations in suspension.

What Triggers Corporations in Suspension

Both the Secretary of State and the Franchise Tax Board have independent authority to cause corporations in suspension, and they suspend for different reasons.

Secretary of State Suspension

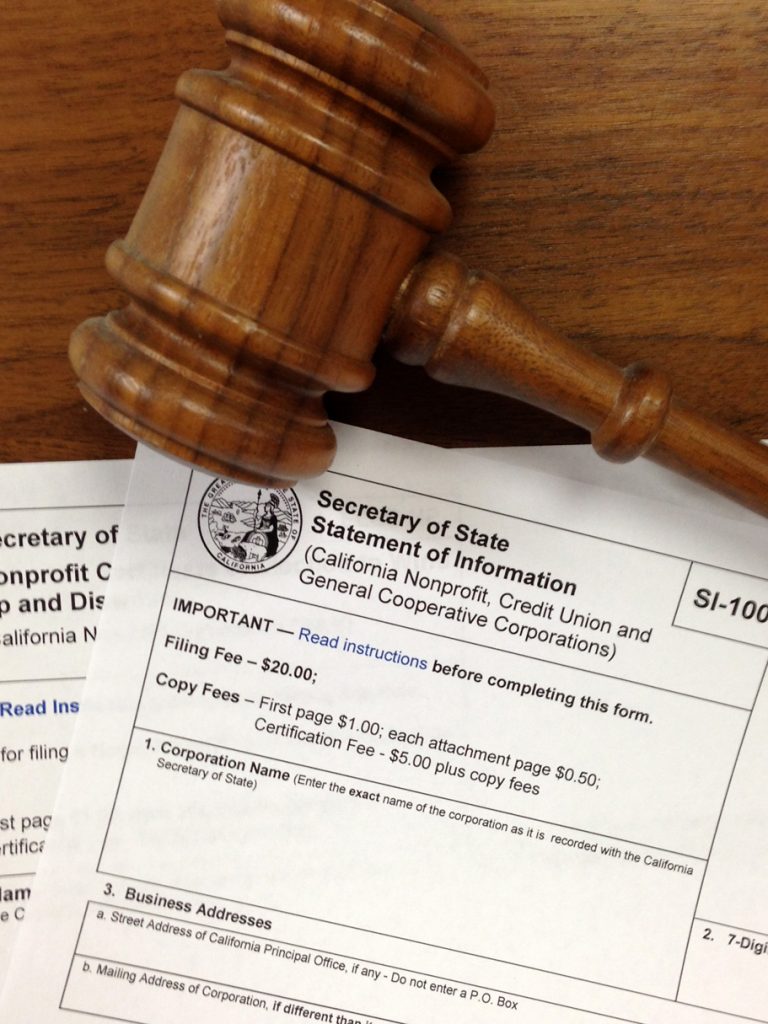

The SOS suspends a corporation for failing to file its Statement of Information — the biennial filing that lists the corporation’s officers, directors, and agent for service of process. Miss the deadline and a delinquency notice follows, with 60 days to file before a penalty is assessed.

Franchise Tax Board Suspension

The FTB suspends a corporation for failing to file tax returns or pay taxes, fees, or penalties owed to the state. Many religious corporations assume this doesn’t apply to them because churches don’t pay income tax — but California tax-exempt status is not automatic just because the IRS has already approved federal 501(c)(3) status. A California nonprofit religious corporation still has its own state filing obligations, and falling behind on those can trigger FTB suspension independent of anything the IRS is doing.

The Real Penalty Amounts

This is where a lot of guidance about corporations in suspension gets it wrong for churches specifically. The commonly cited $250 late filing penalty for a delinquent Statement of Information applies to for-profit corporations and LLCs. Domestic nonprofit corporations — the category most churches fall into — face a $50 penalty under Revenue and Taxation Code §19141, regardless of whether the corporation has tax-exempt status. It’s a smaller number, but the consequences of ignoring the underlying filing are the same.

What Corporations in Suspension Actually Costs You

A suspended corporation isn’t just administratively behind — it legally cannot exercise the powers, rights, and privileges the state grants it. That includes the ability to:

- Sell, exchange, or transfer real property located in California

- Sue or defend itself in court

- Amend its articles of incorporation or formally dissolve

- Enforce contracts entered into during the suspension — the other party can void them at will

A suspended corporation can also lose its own name to another entity during the suspension period, and its state tax-exempt status may be suspended or ultimately revoked along with everything else. For a church mid-transaction, this means escrow can’t close, a purchase agreement can become unenforceable, and a deal that took months to negotiate can stall indefinitely until the corporation’s status is fixed.

How to Get Revived

Resolving corporations in suspension depends on which agency suspended the corporation — and if both did, both processes have to be completed.

SOS Suspension

File the current Statement of Information along with any required fees or penalties. As long as the corporation hasn’t missed two consecutive filing cycles, this alone typically resolves an SOS suspension.

FTB Suspension

File any past-due returns, pay outstanding taxes and penalties, and submit an Application for Certificate of Revivor (FTB Form 3557 BC).

Suspended by Both

File the Statement of Information with the SOS first. That generates a proposed relief letter, which then gets submitted to the FTB along with the Application for Certificate of Revivor. The corporation remains suspended until both agencies have signed off — completing one without the other doesn’t restore good standing.

Before starting any revivor process, confirm the corporation’s current status through the Secretary of State’s bizfile business search, and review the FTB’s own revivor requirements at My Business is Suspended.

If Another Entity Has Taken the Corporation’s Name

If the corporation’s name was reserved or claimed by another entity while it was suspended, the SOS will deny a revivor request until the name issue is resolved. Options are to obtain a release of the name reservation, get written consent to use the name, convince the other entity to change its name, or file amended Articles of Incorporation adopting a new name for the corporation. Choosing a new name means running a name clearance check, reserving the new name, preparing board minutes authorizing the change, and filing the amendment with the SOS along with the required fee.

Related Articles

Church Officer and Director Liability

Choosing the Right Business Entity and Entity Formation

Why Use Bushore Real Estate

Deductible Donations for Congregation Members

Disclaimer: Every situation is different and particular facts may vary thereby changing or altering a possible course of action or conclusion. The information contained herein is intended to be general in nature as laws vary between federal, state, counties, and municipalities and therefore may not apply to any given matter. This information is not intended to be legal advice or relied upon as a legal opinion, course of action, accounting, tax or other professional service. You should consult the proper legal or professional advisor knowledgeable in the area that pertains to your particular situation.

{kind=link}