The Risks of Renting Out Your Church Parsonage in California

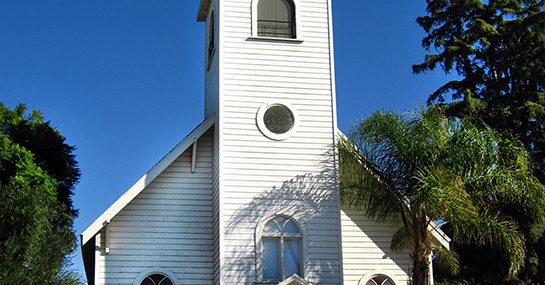

Renting out your church parsonage can risk your property tax exemption and trigger UBIT. Here’s when that happens — and how to protect your exemption.

Renting out your church parsonage can risk your property tax exemption and trigger UBIT. Here’s when that happens — and how to protect your exemption.

Church solar panels now qualify for a federal cash incentive through Direct Pay. Here’s what churches actually pay upfront, how that incentive changes the math, and the financing, billing, and property tax issues to plan around.

Most real estate sales between private parties in California don’t require approval from the Department of Real Estate (DRE). However, DRE oversight may apply when properties are subdivided, interests are offered to the public , or licensed brokers engage in regulated activity.

An affidavit of death is a sworn legal statement used to formally declare that a person has died. It’s typically signed by someone with personal knowledge of the death—such as a family member, executor, or trustee.

Buyer Representation Agreement—a binding contract outlining roles, duties, and expectations. California’s Business and Professions Code §10147.5

California’s SB 1103 gives small nonprofit and business tenants new protections on rent increases, lease translation, and operating cost disclosures. Here’s what churches leasing commercial space need to know.

How churches and property owners can prevent mechanic’s liens through contractor vetting, Preliminary 20-Day Notices, joint checks, and conditional/unconditional lien releases.

Beware of old galvanized plumbing and the potential for leaks and/or poor water pressure caused by corrosion.

Forming a non-profit is easier with a clear plan. Learn the essential steps, filings, and legal requirements to start a compliant nonprofit organization.

Enacted in 1972, the Mills Act encourages the preservation and maintenance of Qualified Historic Structures by reducing property taxes